Introduction

With bitcoin prices falling and energy prices rising, the profit margins associated with bitcoin mining have compressed significantly, likely forcing certain miners to turn off their machines. Similar to past cyclical downturns in crypto, uninformed pundits have begun to posit the uninformed theory that if no miners are able to mine profitably, they turn off their machines and liquidate their bitcoin reserves, adding to further sell pressure. Under this theory, no transactions across the network could then be validated or confirmed, and the value of the network would thus go to zero. However, this is not true.

The actual situation is far more nuanced and in fact, one of Satoshi’s core innovations – the difficulty adjustment – allows the Bitcoin network to naturally absorb and recover from shocks like this. That is, there is an “equilibrium” network hashrate, in which a decrease in the mining “difficulty” facilitates a recovery of mining activity. In that way, mining reflects the broader rise and fall of the credit cycle. We’re seeing this now as bitcoin’s current hashrate is hovering near all-time-highs despite falling revenues. As we will explore in this report, a period of rapid credit expansion from 2020 through 2021 followed by rising capital costs observed in 2022, has accelerated the negative impacts to bitcoin miners in light of declining prices.

In order to better understand these mechanics, it is important to first understand the key inputs that drive profitability for bitcoin miners, which include:

- The technical capabilities of the miner model (i.e. the higher efficiency of newer mining equipment can reduce costs)

- The total network’s average hashrate (a lower network hashrate makes mining less difficult and thus more profitable)

- The power cost per kilowatt hour (kWh) (lower energy costs make mining more profitable and vice versa)

- The price of bitcoin (higher bitcoin prices make mining more profitable and vice versa)

Breakeven analysis

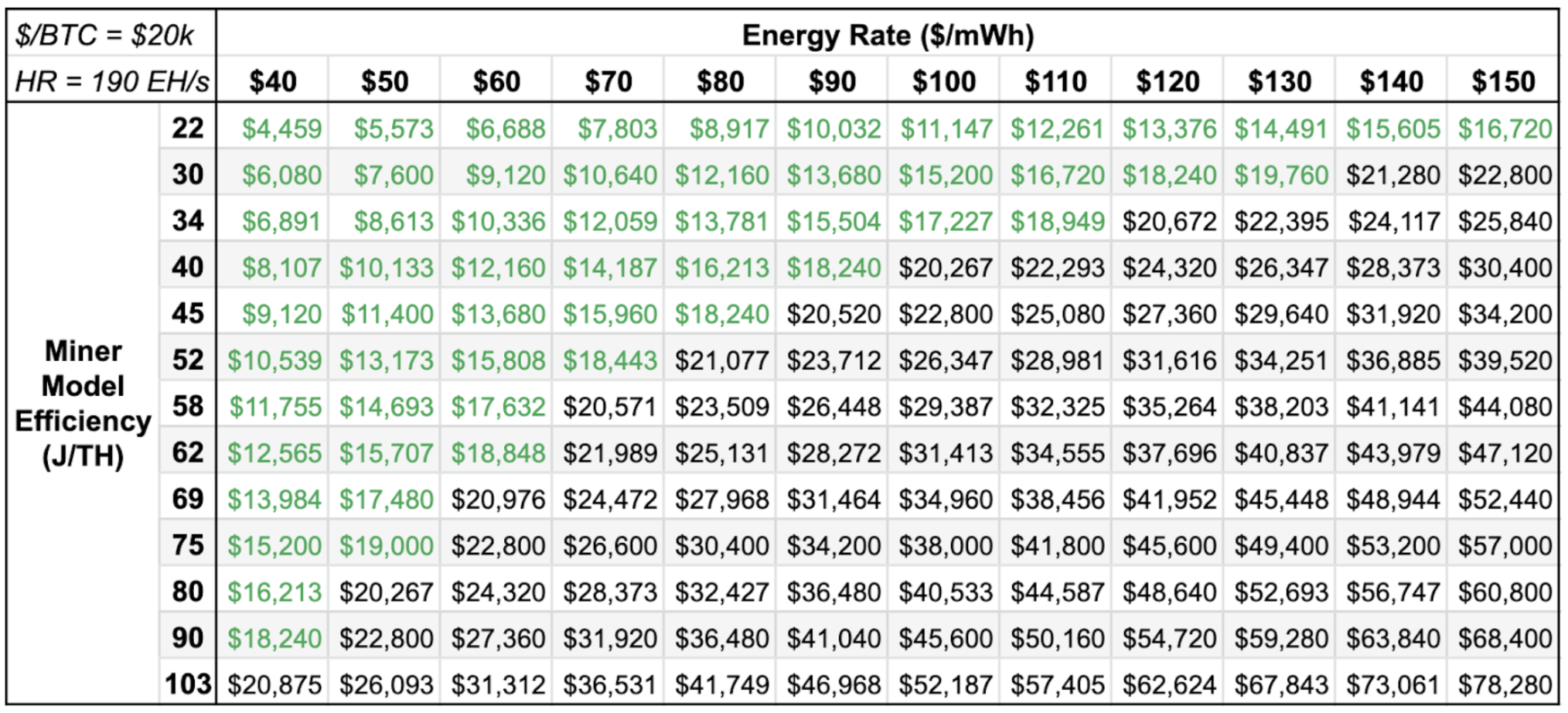

While it may be directionally useful to calculate a “breakeven” cost structure for the average bitcoin miner based on the inputs detailed above, the reality is that two of these inputs – miner model efficiency and energy costs – vary significantly across global mining operations. Further, mining costs can vary depending on a given operator’s labor and capital expenditures including initial outlay for machinery and construction costs, as well as the depreciation schedules of said machinery.

For the purposes of this analysis, we’ve focused on the marginal cost of production, which represents the cost of mining a bitcoin at an already-operational site, assuming machinery is in place and ongoing maintenance costs are minimal. Other forms of cost analysis for miners include inputs for depreciation expenses for application-specific integrated circuits (ASICs) and/or hosting facilities (direct cost of production), as well as overhead costs such as payroll and SG&A (total cost of production).

The table below depicts marginal cost scenarios for various miner models and power costs, based on static inputs for the price of bitcoin and network hashrate (~US$20,000 & ~190 exahashes per second or EH/s).

As this table demonstrates, the currently depressed price of bitcoin and elevated network hashrate (and thus mining difficulty), mean that only the newest generation mining models and/or operations with relatively low power costs can profitably mine bitcoin in the current environment.

The importance of the difficulty adjustment

Because miners rely on the mining reward (consisting of newly created bitcoins and transaction fees) in order to cover operational expenses, a lower bitcoin price dampens the purchasing power of these outputs and makes covering expenses more difficult. As a result, miners with the highest production costs will no longer be profitable and will be forced to stop mining, which is analogous to traditional commodity production cost dynamics. However, unlike traditional commodities like gold, where production costs and operational outlays respond more slowly to changes in the price of gold, the production costs for bitcoin are designed to dynamically adjust to current market conditions every two weeks.

Every 2,016 blocks (approximately every 14 days, an “epoch”), the bitcoin protocol adjusts the difficulty (of mining new blocks) to reflect the average hashrate of that period (a proxy for the amount of computing power attempting to mine the next block). Adjustments are based on a protocol rule which dictates that bitcoin blocks should take ~10 minutes on average to create. If blocks are being created every ~9 minutes on average instead of every ~10 minutes (too easy), the mining difficulty would increase. Conversely, if blocks are being created every ~11 minutes on average (too difficult), the difficulty would be reduced. The difficulty adjustment is a critical component of the bitcoin protocol that not only ensures bitcoin’s strict monetary policy, but allows the network to constantly adapt and absorb shocks related to variability in the aforementioned profitability inputs.

So are miners selling? Does it even matter?

Another common concern during cyclical downturns in bitcoin mining is the extent to which miners are selling their bitcoin holdings. Realistically, regardless of where the market is positioned in a given cycle, there are certain miners with thinner profit margins that are likely selling some portion of their bitcoin-denominated income. In times of market turmoil and a declining bitcoin price, margins compress across the board and naturally force more miners to become net sellers of their bitcoin, whether they are simply trying to weather the storm or shutting down their operations indefinitely. However, even if the entirety of newly issued bitcoin were immediately sold onto the market each day, that would only equate to 900 BTC (or ~US$19M at current prices) of daily sell pressure (or ~0.005% of bitcoin’s total market cap). Further, as a percentage of average daily trading volume of bitcoin across top exchanges (~60k-90k in recent days), the daily new issuance represents only ~1.0-1.5% of total volumes.

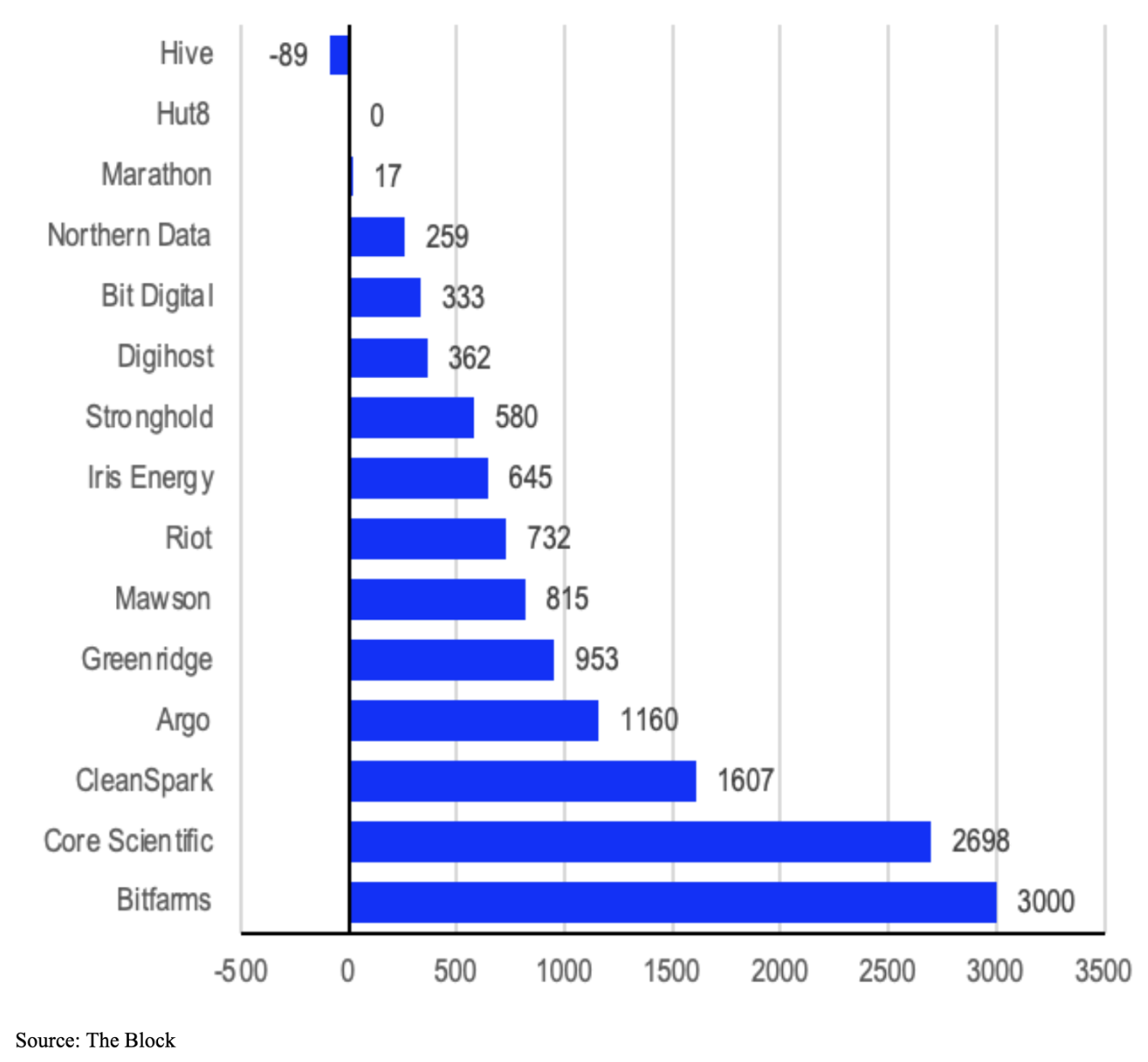

More importantly, sell pressure of greater magnitude is likely to stem from mining operators that are forced to exit the market entirely or liquidate some portion of bitcoin reserves, likely due to being overleveraged or managing operations too close to the margin. Evidence of such selling can be observed via disclosures from some of the largest publicly traded mining companies. From January to May of this year, a cohort of 15 public mining firms reported that they mined nearly 22K BTC, with their holdings increasing from 35K BTC to 47K BTC over the period. This reflects net BTC sales of approximately 10K BTC (according to The Block). This cohort includes mining companies that have maintained consistent BTC liquidation strategies such as Iris Energy, Mawson, Greenidge, BIT Digital and CleanSpark, as well as firms that have recently revised their BTC holding strategies in light of market conditions. Mining firms such as Core Scientific, Marathon, Riot, Bitfarms, Hut8, Argo and HIVE had previously committed to a 100% holding strategy in late 2020 (which served them well throughout a period of price appreciation and robust financing in 2021), but many have been forced to rethink their capital structure in 2022.

Chart 1. Bitcoin liquidations 2022 year-to-date (in BTC)

In May, Core Scientific reduced its bitcoin reserves by 20%, raising approximately US$80M, while Argo and Riot began liquidating portions of their monthly production. Conversely, Marathon has trimmed their reserves marginally, while Hut8 and HIVE have maintained their full holding strategy. Bitfarms liquidated 3K BTC (roughly half of their reserves) in June to deleverage its US$100M outstanding loan from Galaxy. In aggregate, Riot, Core Scientific, Argo and Bitfarms accounted for more than half of the bitcoin sold by this cohort of public companies year-to-date. Unsurprisingly, many of these public mining companies have seen their share prices decline ~75-95% from their 2021 highs.

Chart 2. Share price declines year-to-date (BTC miners)

Credit cycles in the context of bitcoin mining

It is important to note that the landscape for bitcoin mining financing has changed dramatically since prior cyclical downturns, as the amount of lenders offering various forms of liquidity to mining operators has grown rapidly, particularly throughout 2021. In addition to traditional financing methods like issuing common shares, bonds, or convertible notes in the private and public markets, bitcoin mining companies also began to pledge their bitcoin holdings or ASIC mining equipment as collateral for loans from crypto companies like Genesis Capital, NYDIG, Silvergate, Foundry, Galaxy Digital, BlockFi, Securitize and BlockFills (it is worth noting that Coinbase offers loans through its Borrow platform that can be backed by bitcoin, but to date has not made loans backed by mining equipment or future mining revenue). These loans have primarily been structured in an overcollateralized manner and were largely executed by mining operators with aggressive expansion plans during 2021, such as Bitfarms, Marathon Digital, Greenidge, and Core Scientific. Additionally, certain mining operators were able to structure debt agreements based on revenue sharing, typically denominated in bitcoin.

Furthermore, a number of non-crypto-native financial entities issued loans to bitcoin mining companies in 2021 to purchase additional ASIC miners, largely in an effort to expand mining infrastructure and capacity throughout North America in response to the hashrate migration away from China (following their mining ban enforced during the summer of 2021). For example, venture debt firm Trinity Capital signed a senior secured equipment financing term to lend US$30M to Hut8 Mining in December 2021. In June 2021, private credit investment firm WhiteHawk Finance signed a US$40M loan agreement with Stronghold Digital, allowing the mining operator to purchase incremental ASICs. Both of these deals were executed with an annualized interest rate of about 10% (according to The Block).

Based on the financial statements from a cohort of the largest public or private bitcoin mining companies, it is estimated that over US$5.8B was raised by these entities during 2021 (75% of which was equity financing). During October and December 2021 alone, these companies raised roughly US$2.4B, accounting for over 40% of their total capital raised during the year (according to The Block). Debt financing also saw immense growth towards the end of 2021, with convertible notes accounting for the majority of the debt financing in 4Q21, followed by secured loans, senior unsecured notes, and loans secured by bitcoin holdings or ASICs. Marathon Digital, one of the largest public bitcoin mining companies, issued US$747M in convertible notes in November, which is the largest executed debt financing for a bitcoin mining company to date.

Another way to directionally characterize the financing surge in 2021 is by analyzing the dilution of common shares among publicly traded bitcoin mining firms. Marathon, Riot, Argo, HIVE, Bitfarms and Hut 8 all increased the number of their outstanding shares significantly in 2021, following a relatively flat year in 2020. This dilution also happened to coincide with the aforementioned strategic shift within these entities, in late 2020, to hold the vast majority of their mined bitcoin instead of liquidating them to ease operational expenditures.

Given the decline in bitcoin price in recent months and resultant margin compression for mining operators, the financing environment for the industry has shifted materially since late 2021. Raising capital in the public markets has become exceedingly difficult and while private loan activity has continued into 2022, access to financing has meaningfully narrowed in light of the current backdrop. A swath of mining companies who were aggressively expanding their operations over the last 1-2 years and leveraging their balance sheet to do so (knowingly or unknowingly with an assumption of flat to higher bitcoin prices), are now being forced to restructure their operations and in many cases liquidate some portion of their bitcoin reserves to meet regular expenses as well as loan payments or margin calls. These conditions should present opportunities for consolidation across the mining industry in the second half of the year as less prudent miners continue to face challenges, a sentiment which was echoed at a mining panel at the Consensus 2022 conference in Austin, TX earlier this month.

That being said, there is reason to believe that certain miners – particularly those who’ve taken a more conservative approach – have been able to appropriately take advantage of the aforementioned expansion in financing access. All else being equal, more liquid capital markets facilitating incremental infrastructure investment to improve the efficiency of mining operations (via newer equipment and/or lower power costs from renewable or stranded energy sources), should give these players more flexibility during times of stress.

Hedging strategies

Additionally, a more robust bitcoin derivatives market should allow miners even more optionality in terms of potential hedging strategies. One strategy miners would use, if they are wary of declining bitcoin prices, would be to buy put options on the stocks of public mining companies (with strike prices at/near their cost of production), which historically have traded as high-beta plays on the price of bitcoin. Further, in order to fund these option purchases, miners can simultaneously write (sell) covered call options in order to effectuate a costless collar strategy.

Another strategy would be writing (selling) bitcoin futures contracts to hedge spot exposure. A more recent development in terms of strategic hedging is the concept of hashrate derivatives (allowing miners to effectively “long” the prospect of hashrate increasing, as they are inherently “short” hashrate as their profitability rises when the network hashrate declines), but these markets are relatively novel and illiquid. Perhaps the most simplistic method for hedging, however, remains a strategy of consistently liquidating some portion of bitcoin-denominated-income to fiat.

Chart 3. Bitcoin miner net flows of BTC (1m rolling average)

Where are we in the cycle?

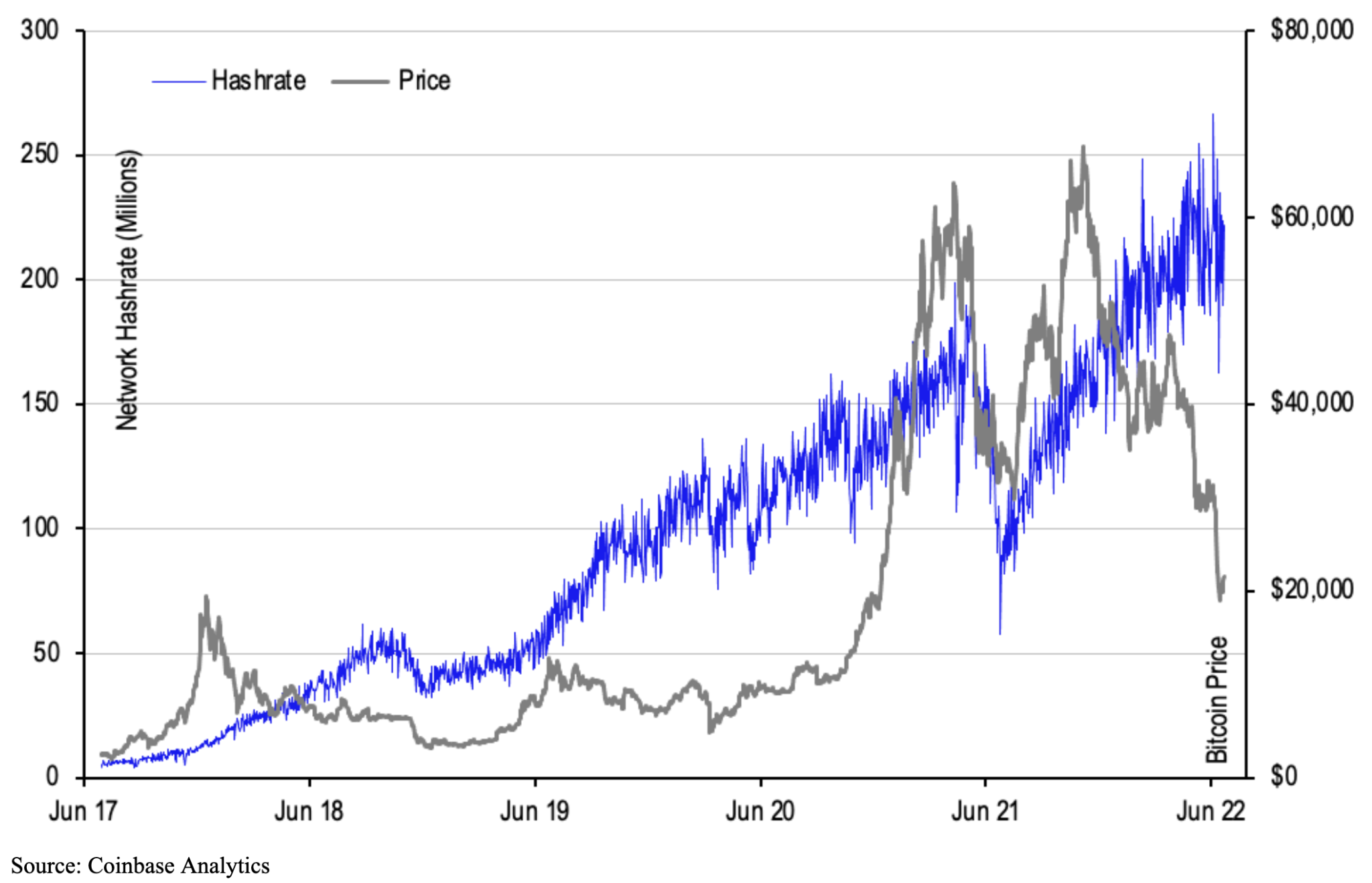

While the bitcoin mining ecosystem has matured significantly since prior cyclical downturns, it is illustrative to analyze past mining cycles in order to estimate where we are in the current cycle. Looking at the period from 2017 to 2019, we can observe a cyclical progression very similar to the trajectory of today. In late 2017, the price of bitcoin began to grow at a faster pace than the network hashrate, which led to an influx of new miners and operational expansion to take advantage of that mismatch (similar to the expansion observed throughout 2021). Then, as the price peaked towards the end of 2017, deployment of new equipment continued which caused network hashrate to continue its upward trajectory (similar to the rising hashrate for most of 2022 despite falling bitcoin prices).

Ultimately, the price of bitcoin took another leg down in November 2018 and at that point many miners became unprofitable and were forced to turn off their machines (similar to 2Q22). It was around this time that network hashrate peaked (around 54 EH/s) and began to decrease as miners shut down and mining difficulty adjusted downward. Network hashrate then found a bottom around 35 EH/s (coinciding with bitcoin price lows just under US$4,000) before beginning its recovery back upwards. Fast forwarding to the ongoing cycle, it appears as though network hashrate peaked in May around 237 EH/s, as it has decreased in recent weeks to around ~200 EH/s (180 EH/s at current).

Accordingly, while the mining market may still be far from an equilibrium in terms of hashrate, evidence of miner selling and halting of activities in recent months are beginning to manifest in the form of a declining network hashrate and ultimately mining difficulty. Should these declining trends continue, we think that the point at which they subsequently begin to flatten could signal the beginnings of a bottoming process, based on the trends observed in the 2018 crypto winter.

Chart 4. Bitcoin price and hashrate over time

Conclusions

Amidst these difficult market conditions, the conservative approach for many mining operators is to liquidate some portion of their bitcoin holdings as prices decline. As unprofitable miners exit, we expect the hashrate to decline and the difficulty to adjust downward, creating a new equilibrium that better supports activity. We view a lower steady state hashrate as a potential bottoming of the cycle, which would then be a precursor for new entrants. As of this writing, the hashrate of the network has continued its recent downward trajectory and currently stands around ~180 EH/s. On June 22, the difficulty of the network experienced a downward adjustment of 2.35%, which supports the notion that miners have been turning off their machines in recent weeks. The next difficulty adjustment is estimated to occur on July 1 and should provide even more clarity on the evolution of this mining cycle. Notably, block times in this new mining epoch which began on June 22 are taking ~10:20 minutes on average and the estimated downward difficulty adjustment for July 1 is roughly 3.4% (according to Braiins). Although subject to change, this metric will be critical to monitor going forward.

We may also see the broader consolidation of the mining industry, as larger, well-capitalized players acquire smaller operators being forced to exit the market. This process appears to be underway, as graphics card prices have steadily declined year-to-date (mostly recently falling ~15% MoM in May, according to Decrypt) and top-of-the-line ASICs are being offloaded on secondary markets at large discounts (in the range of ~65% below highs seen last year). So while we would expect to see various miners continue to sell some portion of their bitcoin holdings or mining equipment in this environment, or even be wholly acquired, we also recognize that this process represents a natural, self-correcting feature (not a bug) of the bitcoin network.